The latest martial arts industry statistics for 2026 show a sport leading a curious double life. Walk past any suburban strip mall, and you’ll find a jiu-jitsu gym or karate dojo sandwiched between a nail salon and a pizza place. Open a financial terminal, and you will find that same strip mall business is part of a $21 billion U.S. industry growing at over 6% a year, feeding into a global ecosystem that includes billion-dollar media rights deals, nine-figure equipment markets, and a professional MMA circuit valued at over $12 billion.

The disconnect between how people perceive martial arts: niche, traditional, local, and what the numbers actually show is why this guide exists.

This is a reference built for people who need the real data: gym owners benchmarking their business, investors sizing an opportunity, operators planning expansion, and marketers building content that ranks. Every statistic here is sourced from primary market research firms, industry databases, and verified business reports from 2024 to 2026. Where figures vary between sources, we note the range rather than cherry-pick the most dramatic number.

What you’ll find in this guide: how the martial arts business statistics break down by market segment; where the MMA industry statistics point for the next five years; which parts of the market are genuinely growing versus stagnating; and what the profitability picture looks like for gym owners at street level.

To understand where the industry sits today, it helps to look at how it got here.

The martial arts industry: from niche to mainstream

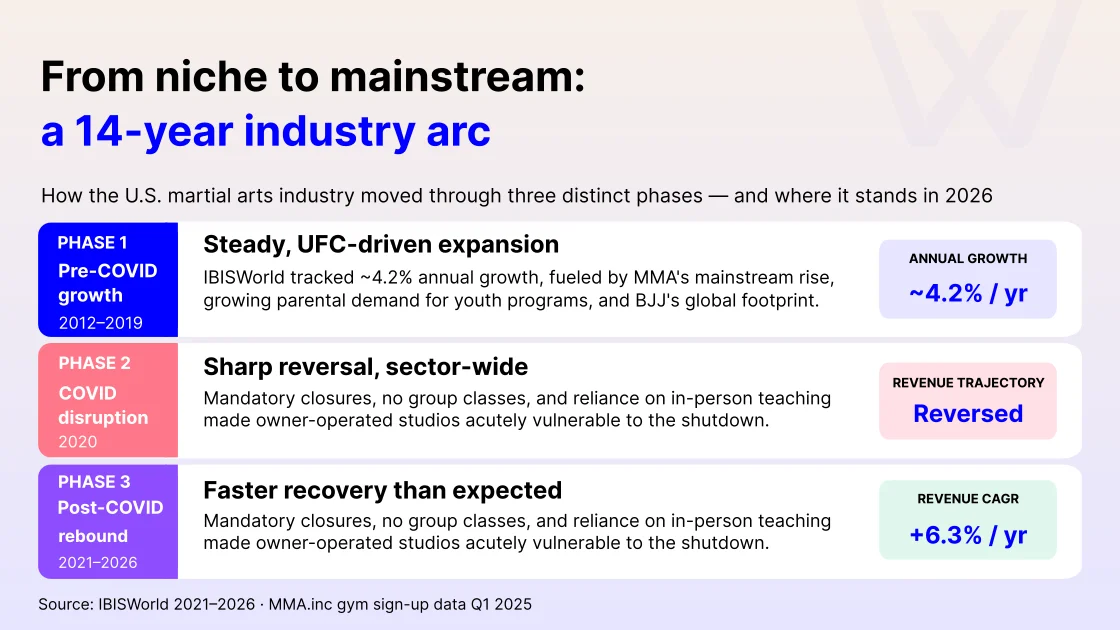

Pre-COVID growth (2012–2019)

The martial arts business statistics tell a clean pre-pandemic story. Between 2012 and 2017, IBISWorld tracked industry growth at approximately 4.2% annually, steady, respectable, and driven largely by the explosion of MMA’s mainstream appeal following the UFC’s rise. By 2019, the U.S. market had established itself as a billion-dollar category with no dominant chain, high entrepreneurial entry, and a participation base spread across dozens of disciplines.

The number of U.S. martial arts enterprises grew 14.2% year-on-year on average between 2012 and 2017, reflecting both the UFC’s cultural halo effect and the growing parental demand for youth development programs. Karate, taekwondo, and BJJ were the three disciplines absorbing most of that growth.

The COVID disruption (2020)

The pandemic hit the industry hard and fast. Mandatory closures shuttered studios for weeks or months, group classes were eliminated, and revenue collapsed. The martial arts studios industry, which had grown strongly for the majority of the five years leading up to 2020, saw that trend abruptly reversed.

Unlike gym chains with deep balance sheets, most martial arts studios are owner-operated small businesses. The absence of recurring revenue models and the dependency on in-person instruction made the sector acutely vulnerable. Studios that survived did so primarily through government relief programs, emergency pivots to outdoor training, and online class offerings held together with Zoom and goodwill.

Post-COVID rebound (2021–2026)

The recovery was faster than most expected. As restrictions eased, martial arts participation rebounded sharply, driven by renewed consumer focus on physical and mental health, pent-up demand from students who had paused training, and a cultural moment that had more people seeking structured, community-based fitness rather than solo gym workouts.

Between 2021 and 2026, U.S. industry revenue grew at a 6.3% CAGR. Business count expanded from approximately 35,000 to over 72,000 studios, a 15.3% CAGR that suggests not just recovery but genuine structural growth. In early 2025, MMA.inc reported a 192% year-over-year increase in gym sign-ups across its platform, covering 30 gyms in four countries.

| 6.3% U.S. revenue CAGR (2021–2026) | 15.3% U.S. studio count CAGR (2021–2026) |

With that growth trajectory in mind, the next question is scale: how big is this market in absolute dollar terms?

Martial arts market size & global overview

The U.S. market: scale and structure

The U.S. is the most thoroughly documented and the largest single market in the global martial arts industry. IBISWorld’s 2026 figures place total U.S. martial arts studios revenue at $21.0–21.2 billion, confirming the industry’s position well inside the top tier of specialty fitness categories.

That $21 billion figure covers membership revenue, supplementary services, and in-studio retail. It does not capture the parallel markets for equipment, apparel, events, media rights, and digital products, meaning the real addressable market for anyone operating in or investing in martial arts is significantly larger than any single data point suggests.

Average monthly tuition sits at approximately $150 per student. That pricing places martial arts above budget tiers like Planet Fitness, but well below premium boutique fitness. It is the kind of price point that parents pay for their children without much deliberation, but that adult hobbyists revisit quickly when household budgets tighten.

Global martial arts market size

Global projections vary by scope, but the directional consensus is clear. The combined global martial arts industry, training, equipment, events, apparel, and digital, is projected to reach $170 billion by 2028, reflecting a 7.9% CAGR. That includes everything from village dojos in Japan to UFC pay-per-view revenues to the global market for rash guards and shin guards.

For comparison, the global gym and fitness industry generated an estimated $116 billion in revenue in 2024 (per IHRSA) and is projected to exceed $200 billion by 2030. Martial arts, by this measure, sits at roughly 15% of the entire global fitness industry when its full scope is counted, a meaningful share of a much larger category.

Industry insight

The $170 billion global projection includes segments that rarely appear in martial arts market size discussions, media rights, streaming platforms, apparel licensing, and sports tourism. Studio owners are operating inside a much larger ecosystem than their membership roster would suggest.

Industry segmentation at a glance

| Segment | Example sub-markets | Growth signal |

| Training facilities | Traditional dojos, MMA gyms, hybrid studios | 6.3% CAGR (U.S.), steady, mature |

| Professional events | UFC, ONE Championship, PFL, Bellator | 8–12% CAGR, high growth via media |

| Equipment & protective gear | Gloves, pads, bags, headgear | 4.6–6.0% CAGR, consistent demand |

| Martial arts apparel | Gis, rash guards, shorts, branded wear | 4.0% CAGR, emerging premiumization |

| Digital platforms | Online coaching, apps, subscription content | Early stage, rapid but unquantified |

Market size tells you the dollars. Participation tells you who is actually generating them.

Martial arts participation rate: Who is training

U.S. participation numbers

Approximately 18 million Americans participate in martial arts annually, spanning disciplines from MMA and BJJ to taekwondo and karate. That figure comes from Glofox and WodGuru’s 2025–2026 industry reports and is consistent with Statista’s separate estimate of 3.9 million actively engaged participants in the martial arts sector specifically, a number that likely reflects committed regular practitioners rather than occasional students.

Youth dominance: Why under-18s drive the business

Around 40% of all martial arts participants in the U.S. are under 18. This is not incidental; it is structural. Parents enroll children for discipline, focus, confidence, and physical fitness. The value proposition is compelling and relatively recession-resistant: parents are far less likely to cancel a child’s martial arts membership than their own gym membership when cutting household expenses.

Parents typically spend $100–$300 per child on martial arts classes. Studios offering family membership plans report up to 25% higher retention rates than those pricing per individual, because once a family is embedded, the switching cost is social, not just financial.

Academically, the research attention on youth is growing just as fast as participation. More than 60% of recent martial arts research papers focus on youth participants, compared with less than 20% of studies published before the mid-1990s.

Business insight

Studios without a structured youth program are leaving their most stable revenue stream on the table. A child who starts at age 7 and stays through their black belt at 14 represents $12,000–$25,000 in lifetime membership value before a single adult class is sold.

Gender breakdown and female growth story

The martial arts participation rate among women has shifted meaningfully over the past decade. Women now account for 30–40% of all participants, up from roughly 20% ten years ago. The growth is concentrated in kickboxing, BJJ, Krav Maga, and Muay Thai, driven primarily by self-defense demand and the functional fitness reputation these disciplines have built.

In the MMA equipment market specifically, the female segment is projected to grow at a 5.23% CAGR through 2030, faster than the male segment and faster than the overall market. That trajectory in purchasing behavior tends to precede participation growth, suggesting female enrollment will continue rising even beyond current projections.

| Demographic | Estimated share | Trend (2026 outlook) |

| Male (all ages) | 60–70% | Stable, dominant segment |

| Female (all ages) | 30–40% | Fastest-growing, 5.23% CAGR in equipment |

| Under 18 | ~40% of total | Strong, parent-driven enrollment |

| Adults 18–45 | Core adult segment | Driven by fitness & MMA media exposure |

| Adults 50+ | Small but growing | Tai chi, aikido, low-impact styles |

Income demographics

Pew Research data from its 2023 surveys indicates that households earning $50,000–$100,000 annually are the most likely to enroll in martial arts programs. This middle-income skew has real implications for pricing strategy. Studios pitched too far below this bracket undervalue their service to cover instructor costs. Those pitched above it narrow their addressable market without a compelling premium offering to justify it.

Zooming in from participants to the businesses serving them, the studio-level picture reveals a fragmented but resilient industry.

Martial arts studio & gym industry statistics

Market fragmentation: a 72,000-business industry with no clear leader

The martial arts gym industry statistics reveal a structural paradox: the sector is large enough to be a serious financial market, but fragmented enough that no single player controls even 5% of it. IBISWorld confirms there are 72,029 martial arts studio businesses in the U.S. in 2026. The most successful franchise networks hold approximately 1.8% of total market share, a figure that illustrates how thoroughly independent and locally driven the industry remains.

This fragmentation creates both opportunity and challenge. There is no dominant incumbent to displace. A well-run independent studio can compete directly with franchise operations on quality, community, and instructor reputation. But it also means most studios operate without the infrastructure, marketing scale, or procurement leverage that chains enjoy.

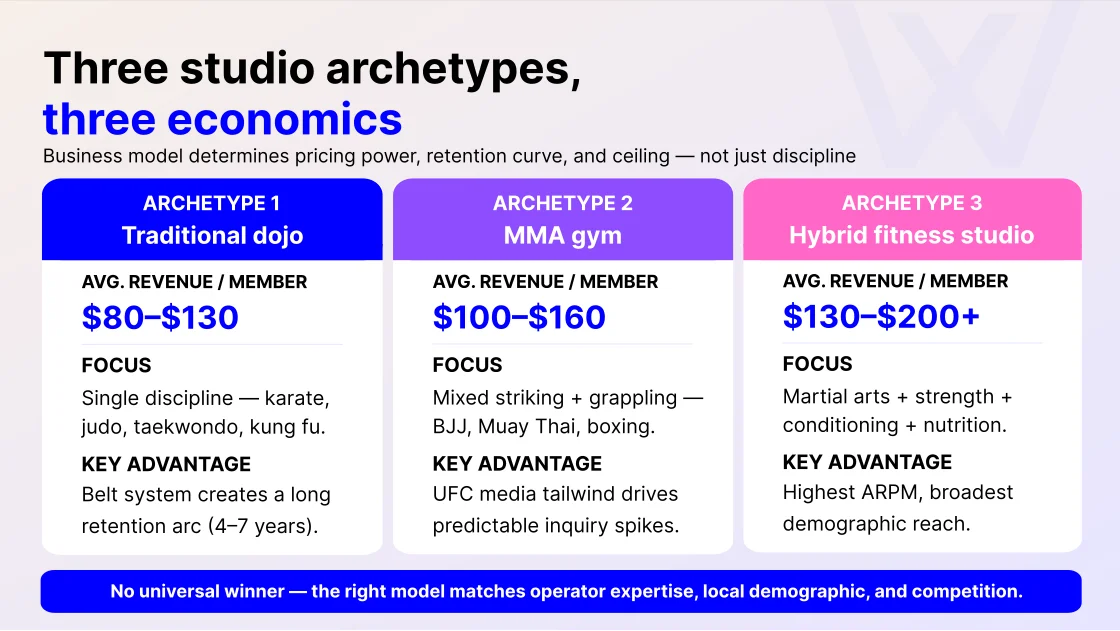

Business models: three distinct archetypes

Three models dominate the studio landscape, each with different economics and student demographics.

| Model | Focus | Typical ARPM | Key advantage |

| Traditional Dojo | Single discipline: karate, judo, taekwondo | $80–$130 | The belt system creates a long retention arc |

| MMA Gym | Mixed striking + grappling disciplines | $100–$160 | Media tailwind from UFC attracts the adult male demo |

| Hybrid Fitness Studio | Martial arts + strength + conditioning | $130–$200+ | Broadest demographic appeal; highest ARPM (Average Revenue Per Member) potential |

Traditional dojo

Traditional dojos focus on one art, usually karate, taekwondo, judo, or kung fu, and build their business around the belt progression system. ARPM typically lands in the $80–$130 range, lower than other models, but compensated by significantly longer student lifetimes. A child who starts at white belt and trains toward a black belt represents a 4–7 year customer relationship, which is unusual in any fitness category.

The economic strength of this model is predictability. Belt testing fees, uniform sales, and tournament participation create secondary revenue layered on top of monthly tuition. The structural weakness is demographic concentration: traditional dojos skew heavily toward youth (often 70%+ of enrollment), which makes them vulnerable to local school district shifts, demographic changes, and adult market neglect. Studios in this category that fail to build a parallel adult program tend to cap at 200–250 students regardless of marketing spend.

MMA gym

MMA gyms blend striking (boxing, Muay Thai, kickboxing) with grappling (BJJ, wrestling) and benefit directly from UFC media exposure. ARPM runs $100–$160, with adult students forming the majority of the membership base. The business advantage is media tailwind: every major UFC card produces a measurable spike in inquiries, and studios with a strong digital presence convert that spike into trial classes consistently.

The economic challenge is retention. Adult MMA students drop off faster than traditional dojo students because the entry experience is harder, the injury rate is higher, and the belt/level progression is less defined in some sub-disciplines. Monthly churn at MMA-focused gyms commonly runs 8–12%, compared with 5–8% at traditional dojos. The studios that succeed in this category build structured beginner programs (fundamentals classes, no-sparring tracks for new students) that bridge the gap between fan and committed practitioner.

Hybrid fitness studio

Hybrid studios combine martial arts instruction with strength training, conditioning, and often nutrition coaching. ARPM is the highest of the three models at $130–$200+, and in premium urban markets can exceed $250. The demographic is broader, more women, more general-fitness consumers, more lapsed CrossFit members looking for the next functional training format.

The advantage is the total addressable market. A hybrid studio competes for the CrossFit, F45, Orangetheory, and boutique gym budget, not just the martial arts budget. The challenge is operational complexity: hybrid studios need broader instructor expertise, more equipment investment, longer programming hours, and tighter scheduling logistics. These are also the most software-dependent of the three models; automation is functionally non-negotiable once a hybrid studio passes 150 active members.

Which model wins?

There is no universal winner. Traditional dojos have the most stable cash flow. MMA gyms have the highest growth ceiling when media tailwinds align. Hybrid studios have the highest ARPM and the broadest market. The right model is the one that matches the operator’s expertise, the local demographic, and the realistic competitive landscape, not the one with the highest theoretical margin.

Scale is one question. Whether individual operators inside that scale can actually make money is another.

Is the martial arts business profitable? A data view

The revenue math for a typical studio

Raw market size tells you the industry is big. Profitability data tells you whether individual businesses within it can actually make money. The simplest answer is yes, but the margins are tighter than most people entering the industry expect.

A martial arts gym needs approximately 187 members paying $150 per month to cover the fixed overhead of around $22,441 per month, assuming an 80% gross margin on services delivered. That gross margin sounds healthy until you subtract fixed labor costs, instructor pay, which is the largest single cost line, plus rent, insurance, software, marketing, and equipment maintenance.

80-84% typical gross margin for a martial arts studio (before fixed overhead)

Operating profit margins are far thinner. Net profit margins at the studio level commonly sit in the 7–15% range for businesses that are actively managed. Under-managed studios, those not tracking key metrics weekly, frequently operate below 7% or at a loss despite healthy-looking enrollment numbers.

A 300-student school charging $118 per month grosses $35,400. A 150-student school charging $250 per month grosses $37,500, and almost certainly costs less to run. Smaller and better-priced consistently beats larger and underpriced. That is the core profitability lesson the martial arts business statistics keep surfacing.

The real profitability lever: Student retention

Retention is not a soft metric. It is the single most powerful driver of studio profitability, and most gym owners are not tracking it precisely enough to manage it effectively.

“Churn cost is the total revenue you lose when a student quits. If a student pays $150 per month and the average student stays 14 months, every dropout costs you roughly $2,100 in future revenue. Beyond that, it costs five to seven times more to acquire a new student than to keep an existing one.” —West End Martial Arts Owner

At a 12% monthly churn rate, the average student stays just 8.3 months. With a customer acquisition cost (CAC) payback period of roughly 4 months, a studio is generating net profit on each student for only 4.3 months before they leave. That leaves almost no room for error in pricing, programming, or operational quality.

| Retention benchmark | Monthly churn rate | Average student lifetime | Revenue risk per dropout |

| Poor | >12% | <8 months | $1,200–$1,800 |

| Average | 6–10% | 10–16 months | $1,500–$2,400 |

| Excellent | <5% | >20 months | Risk is low; LTV is high |

Billing friction alone accounts for 23% of student churn, according to Kombat Evolve’s 2025 data. Failed or complicated payments are not a technology inconvenience; they are a revenue hemorrhage.

Studios using automated payment processing and proactive communication systems report 31% higher retention rates, which compounds significantly into annual revenue differences of $20,000–$50,000 for a mid-sized studio.

Profitability Tip

The single highest-ROI investment for most martial arts studios is not marketing spend, it is a martial arts management software platform like Wellyx that automates billing, tracks attendance, and triggers re-engagement messages for at-risk students. The cost is typically $100–$300 per month. The retention improvement pays for it many times over.

The 5-step retention framework for martial arts studios

Step 1: Audit your current monthly churn rate. Most studio owners know their enrollment number but cannot state their monthly churn to the nearest percentage point. Pull the last 12 months of cancellations divided by the average active membership. If the number is above 8%, retention is the single biggest lever on your P&L.

Step 2: Identify your top three drop-off points. Churn is not evenly distributed. Map when students leave: first month, three months, post-belt-test, post-summer-break. The pattern tells you where your curriculum, community, or communication is failing. Most studios will find two or three specific windows that absorb the majority of cancellations.

Step 3: Automate billing and payment recovery. Billing friction alone accounts for 23% of student churn. Failed cards, forgotten updates, and manual invoice chasing are recoverable revenue. Automated retries, dunning sequences, and card-on-file updates close this gap without adding instructor workload.

Step 4: Build at-risk re-engagement flows. A student who misses three classes in a row is 40–60% more likely to cancel than one with consistent attendance. Trigger a head-coach SMS at day 10 of inactivity, a phone call at day 21, and a discounted comeback offer at day 30. The cheapest reactivation is one that happens before the student has emotionally quit.

Step 5: Track lifetime value (LTV) per cohort. Break your student base into cohorts by join month and track average tenure. Cohorts that joined through referral typically retain 40–60% longer than cohorts from paid ads. Once you know your LTV by acquisition channel, your marketing spend becomes a calculation, not a guess.

Insight

The single biggest mistake gym owners make is thinking they have a sales problem when they actually have a retention problem. You can’t out-market a leaky bucket.” — Owner of West End Martial Arts

Case study: what better retention looks like on P&L

Case 1: Mid-sized BJJ academy, U.S. Midwest (~180 active students)

The academy was running monthly churn at 11% before migrating from a manual spreadsheet-and-Stripe setup to a dedicated gym management platform in late 2023. Over the following 12 months, automated billing retries and at-risk-student alerts reduced failed-payment-driven cancellations materially. Monthly churn settled at 6.8%. On a $145 average membership fee, that 4.2-point improvement represented roughly $37,000 in retained annual revenue, before accounting for downstream LTV gains from students who stayed long enough to buy gear, enter competitions, or upgrade to private lessons.

Case 2: Multi-discipline MMA gym, UK (~220 active students)

This gym introduced a structured re-engagement flow for any student missing three consecutive classes, an automated SMS from the head coach at day 10, a manual phone call at day 21, and a discounted comeback week at day 30.

Within six months, dormant-student reactivation rose from under 8% to 19%. The owner reported the biggest single impact was not the discount offer, but the day-10 text, which caught students before they had mentally canceled their membership.

Secondary revenue: Where most gyms leave money

Membership dues are not the ceiling; they are the floor. The most profitable studios in the sector build stacked revenue across private lessons (highest margin per hour), retail gear and uniform, belt testing fees, seminars and workshops, competition team programs, and corporate self-defense training.

Studios without a structured retail offering are surrendering 15–25% of potential monthly revenue per student to online retailers and third-party stores. A student who buys their gi, their gloves, and their shin guards from your studio rather than Amazon is worth materially more per month than their membership fee alone suggests.

Beyond the studios, the professional tier of the sport has its own economics, and the spillback into grassroots enrollment is measurable.

MMA industry statistics: The professional tier

UFC market size and valuation

The UFC’s financial story is one of the most dramatic in sports business. In January 2001, two casino executives, Frank and Lorenzo Fertitta acquired the company for $2 million through their newly formed parent entity, Zuffa LLC. At that point, MMA was banned or unregulated in a majority of U.S. states, and the UFC’s brand was so tarnished that even the new owners attorneys called the deal “buying nothing”. Today, TKO Group Holdings, the parent company combining UFC and WWE, is valued at over $27 billion. UFC alone is worth an estimated $12.1 billion.

In 2024, the UFC generated record annual revenue of approximately $1.4 billion, a 9% year-over-year increase. TKO projects $4.63–4.69 billion in combined company revenue for 2025, driven in part by a landmark $7.7 billion media deal with Paramount starting in 2026. That media contract alone exceeds the entire annual revenue of most professional sports leagues.

Media rights are the engine. Of UFC’s 2024 revenue, $879.4 million, approximately 62.5% of the total, came from media rights and content distribution. Ticket sales, sponsorships, and merchandise make up the remainder.

This revenue structure means the UFC’s primary business is now a media company that happens to produce fights, not a fighting organization that happens to generate media income.

The professional MMA market beyond UFC

| Promotion | Revenue (2024/2025 est.) | Geographic focus | Key differentiator |

| UFC (TKO Group) | ~$1.4B (2024) | Global, U.S.-dominant | Media rights; ESPN deal, PPV dominance |

| ONE Championship | ~$200M (2025) | Asia-Pacific | Weekly fight series: MMA + Muay Thai + Kickboxing |

| PFL | $100M+ (2024 first) | Global expansion, 75%+ outside the U.S. in 2025 | League format; $1B valuation |

The grassroots effect

Professional MMA does not just entertain, it recruits. Every high-profile fight card generates a measurable spike in gym inquiries, class sign-ups, and equipment sales at the grassroots level. MMA.inc reported a 192% year-over-year increase in gym sign-ups in the first quarter of 2025, with 560+ participants joining across 30 gyms in the U.S., Europe, Australia, and New Zealand. The platform now supports over 50,000 active students across 18,000 gyms in 16 countries.

The aspirational pipeline from fan to hobbyist to committed practitioner is real and consistent. UFC viewership, averaging approximately 509,000 viewers per event with a 450-million-strong global fan base, feeds grassroots enrollment in a way that no other sport-to-studio pathway in fitness does with the same reliability.

Membership is only one revenue layer. The gear that participants buy adds another billion-dollar dimension to the industry.

Martial arts equipment & apparel market

Equipment market size and trajectory

Multiple research firms track the global MMA equipment market with slightly different scopes. Straits Research values the global MMA equipment market at $1.5 billion in 2024, projecting growth to $2.25 billion by 2033 at a 4.65% CAGR. IMARC Group places the 2024 figure at $1.5 billion, with a forecast of $2.13 billion by 2033. Fact.MR, using a narrower product scope, estimates $631.5 million in 2025, growing to $1.13 billion by 2035 at a 6.0% CAGR.

The range reflects definitional scope, whether you include all combat sports gear or MMA-specific equipment, but the compound growth consensus is clear: 4.5–6.0% annually through the early 2030s.

Equipment market signal

North America commands approximately 32.85% of global MMA equipment revenue. Europe is tracking towards the fastest regional growth at a 5.81% CAGR through 2030, driven by regulatory harmonization and expanding professional circuit activity. Online channels are growing at 6.03% CAGR, outpacing offline retail for the first time.

What is selling and why

Gloves remain the largest-selling product category across the MMA equipment market, according to a finding consistent across IMARC, Mordor Intelligence, and Straits Research. They are mandatory for sparring, wear out regularly, and are the first purchase new students make. Protective gear (shin guards, headgear, mouth guards, hand wraps) follows as the second largest category.

Premium products are gaining ground on mass-market gear. While mass-market products captured 63.48% of revenue in 2024, the premium segment is projected to post a 5.66% CAGR through 2030, faster than mass-market growth, indicating an upmarket shift in consumer preferences as the participation base matures.

Apparel: slower growth, steady demand

The global martial arts wear market is projected to grow at 4.0% CAGR between 2023 and 2030, with demand rising across gis, rash guards, shorts, and branded athletic wear. North America leads in absolute revenue; Asia-Pacific is projected to grow fastest through 2030. The dominant material is cotton-silk blends, which have been the standard for gi construction for decades.

Understanding the numbers is one thing; understanding what’s pushing them is another.

Key growth drivers in the martial arts industry

The fitness convergence

Martial arts have completed a migration from niche combat sport to recognized fitness modality. The same consumer who might have signed up for a CrossFit box in 2015 is signing up for a BJJ academy or a Muay Thai gym in 2025. The appeal is the same, functional movement, community, measurable progression, but martial arts adds a self-defense dimension that no other fitness category can replicate.

UFC Gym Group’s 2025 expansion targets 150+ locations globally, projecting $7 million in annual revenue from structured warrior training programs. This institutional scaling treats MMA as a fitness product, not a combat sport, and it is working.

Technology: The structural dividing line

Studios without automation are structurally disadvantaged in retention and scaling. This is not a prediction; it is already happening. The gap between studios using dedicated martial arts management software and those using spreadsheets or manual tracking is measurable in retention rates (31% higher with automated check-ins), revenue per member, and lead conversion.

Beyond operations, AI-driven coaching tools, wearable tech that tracks training load and technique, and digital curriculum platforms are entering the market. These tools lower instructor dependency risk and create additional touchpoints that keep students engaged between classes.

Media and pop culture acceleration

MMA has an unusually direct pipeline from viewership to participation. A teenager watching a UFC card on Saturday night googles ‘BJJ classes near me’ on Sunday morning. That search-to-enrollment funnel is well-documented by martial arts studio owners and is one reason the industry’s business count grew 15.3% CAGR between 2021 and 2026, even as the broader economy faced headwinds.

Streaming platforms have amplified this further. UFC Fight Pass, ONE Championship on Amazon Prime, and the PFL’s distribution deals have made professional martial arts accessible to audiences who would never pay for a linear cable package. Global fan base estimates for MMA alone exceed 450 million, a pool that generates steady demand for grassroots training.

Not every signal is a tailwind. Several structural challenges are shaping which studios scale and which stall.

Challenges facing the martial arts industry

The average annual retention rate across health clubs sits at 71.4%, according to IHRSA, meaning roughly one in three members leaves each year. Martial arts studios are not materially different. Approximately 50% of new students quit within their first six months, before they have developed enough skill or community connection to stay committed through the inevitable plateaus.

| Discipline | Average retention | Excellent benchmark | Common drop-off point |

| BJJ | 70–80% | >85% | After 3 months, an early plateau |

| MMA | 65–75% | >80% | After 2 months, the expectations mismatch |

| Muay Thai | 68–78% | >82% | After the belt/level system milestone |

| Karate | 72–82% | >87% | After the initial belt progression slows |

| Taekwondo | 70–80% | >85% | Post-black belt, loss of milestones |

Risk Signal

Families that train together show 90% higher retention, according to Kombat Evolve research. Yet most studios have no systematic strategy to convert a child’s enrollment into a family membership. That conversion gap is costing studios thousands in annual revenue per family that trains partially rather than fully.

Common mistakes martial arts studios make with their numbers

Confusing gross revenue with profitability. A studio grossing $35,000 a month looks healthy until you subtract rent, instructor payroll, insurance, software, and marketing. Owners who benchmark success on top-line revenue rather than operating margin consistently overestimate the financial health of their business. The number that matters is what lands in the bank after the 15th of the month.

Ignoring churn as a lagging indicator. By the time a student formally cancels, they have usually been disengaged for weeks. Monthly churn rate is a rearview-mirror number. Studios that manage retention proactively track leading indicators, attendance frequency, class participation rate, and engagement with communications, so they can intervene before a cancellation email arrives.

Under-pricing youth programs. Youth enrollment is the most stable revenue in the business, yet most studios price children’s classes at or below adult rates out of accessibility concerns. A $140 youth membership with a 2–3 year average tenure is worth materially more than a $160 adult membership with a 9-month tenure. Pricing should reflect LTV, not perceived fairness.

Treating retail as optional. Every student buys a gi, gloves, shin guards, rash guards, and replacement gear throughout their training life. Studios without a structured retail offering send that 15–25% of wallet share to Amazon. A well-run pro shop adds margin without adding mat time, and doubles as a visible brand signal for prospective students touring the facility.

Instructor dependency

Most martial arts studios are built on the reputation of one instructor. When that person is sick, injured, unavailable, or eventually moves on, the studio does not just lose an instructor; it risks losing the membership base that enrolled specifically for them. Studios without team-based instruction models, documented curriculum systems, and a brand identity independent of any individual are one resignation letter away from a retention crisis.

This is not a theoretical risk. Only about 2% of students who begin training at a martial arts school reach the black belt. The attrition happens gradually, and instructor personality, the sense of personal connection to the head coach, is one of the primary variables that determines who stays and who leaves at each stage.

Pricing pressure and economic sensitivity

At an average of $150 per month, martial arts instruction positions itself above budget fitness but below premium wellness. In stable economic conditions, this is a defensible price point. In tighter conditions, and 2024–2025 saw meaningful consumer budget pressure in most Western markets, martial arts can be categorized as discretionary by households that would not categorize their gym membership the same way.

The industry has no dominant chain with pricing power, no universal membership model, and no collective marketing budget. Each studio competes locally on its own, which means pricing discipline and value communication are entirely the responsibility of individual owners.

Looking ahead, several trends are reshaping the competitive landscape into the back half of this decade.

Emerging trends in the martial arts industry (2025–2030)

Hybrid training models

The fastest-growing studio format combines martial arts with strength and conditioning. These hybrid gyms attract people who want functional training outcomes: fitness, athleticism, body composition, and are agnostic about whether they train in a gym. Average revenue per member in hybrid models tends to be higher, and churn lower, because the offering is broader than any single discipline.

Female-focused programming

Women’s participation is growing faster than the overall martial arts market, and purchasing behavior in the female equipment segment suggests that gap will widen. Studios designing female-specific onboarding pathways, timetabling women-only sessions, and building cohort-based self-defense programming are gaining measurable competitive advantage in retention and referral rates. This is not a niche accommodation; it is a primary growth channel.

Digital and hybrid training

Hybrid delivery, combining in-person training with on-demand and live-streamed content, has moved from a pandemic workaround to a standard feature of competitive studios. Subscription-based digital content opens a revenue stream independent of physical mat space. It builds engagement with prospective students who are not yet ready to commit to an in-person membership.

Premiumization

The market is bifurcating. Budget studios compete on price and lose on experience. Premium studios invest in facility quality, instructor credentials, curriculum depth, and community programming, and charge $180–$250 per month without significant resistance from their target demographic. The middle is getting squeezed: studios priced at $120–$140 per month without a strong community or curriculum differentiation are the most vulnerable segment.

Structured youth curriculum systems

Youth martial arts is professionalizing. Studios adopting formal curriculum frameworks, age-appropriate class structures, a digital belt-tracking system, and parent communication platforms are achieving meaningfully better retention than those running informal youth programs. The formalization creates visible progress milestones that keep both students and parents engaged across multi-year training journeys.

Regional martial arts market insights

| Region | Market status | Key drivers | Watch for |

| North America | Largest market | 72,000+ studios; UFC media tailwind; MMA gym growth | Market saturation in urban cores |

| Asia-Pacific | Fastest-growing region | ONE Championship expansion; cultural tradition; growing middle class in India, Indonesia, Vietnam | Rapid gym build-out; AI coaching adoption |

| Europe | Strong growth, BJJ & MMA leading | PFL: 75%+ of events outside U.S. in 2025; UK MMA surge; EU regulatory harmonization | Equipment: 5.81% CAGR, fastest regionally |

| Middle East | Emerging hub | UFC $50M Abu Dhabi training facility; PFL MENA launch; government sports investment | Event hosting frequency is increasing fast |

| Latin America | High cultural engagement | BJJ’s Brazilian origins create an authenticity premium; MMA is deeply embedded | Digital access expansion driving online training |

High retention is an indicator that your school is performing well, and your students are happy with your services. Both churn rate and retention rate tell the same story, but from different angles.

Wrap up

Taken together, these martial arts industry statistics confirm one thing clearly: this is a large, structurally growing, and commercially underestimated industry at every level.

What the data actually means

Martial arts is a fitness business with a combat veneer

The majority of students who walk into a martial arts studio in 2026 are not there to fight. They are there for fitness, stress management, community, and a sense of progression that traditional gym workouts do not provide. The studios that understand this, and market accordingly, are growing faster than those pitching combat technique above all else. Outcome-based messaging (confidence, fitness, discipline, stress relief) converts a wider demographic than discipline-specific messaging.

Youth revenue is the most stable revenue

Youth enrollment behaves differently from adult enrollment in one important way: the decision-maker (the parent) and the dropout-risk party (the child) are different people. A child rarely cancels their own membership. Parents cancel, but they cancel far less frequently than adult hobbyists who can rationalize skipping class. Studios with robust youth programs have fundamentally more stable cash flows than those reliant on adult discretionary enrollment.

Most studios are under-monetizing

The average martial arts studio collects membership fees, occasionally charges for belt tests, and sends students to Amazon when they need gear. The most profitable studios treat membership as the floor, not the ceiling: stacking private lessons, retail, event revenue, digital content, and corporate programs above it. The operational complexity of managing multiple revenue streams is exactly why martial arts management software is no longer optional, it is the infrastructure that makes diverse revenue feasible to run.

Bottom line

For studio owners, the opportunity is clear, but so is the discipline it requires. Retention, not enrollment, is the real lever. Diversified revenue beats membership-only models. And technology is no longer a back-office nicety; it is the operational foundation that separates studios that scale from those that stall.

The data is the starting point. What you build with it is the differentiator.

If you’re running a martial arts studio and want to put these benchmarks to work, tracking churn, automating billing, and converting one-off students into long-term members, explore Wellyx’s martial arts studio management software to see how the operational layer behind these numbers actually works in practice.

Frequently Asked Questions

How big is the martial arts industry?

The U.S. martial arts studios market is valued at $21+ billion in 2026, per IBISWorld. Globally, the combined industry, covering training, events, equipment, apparel, and digital, is projected to reach $170 billion by 2028. It is a larger category than most people outside it assume.

Is the martial arts industry growing?

Yes. U.S. revenue has compounded at 6.3% annually over the past five years. Business count has grown even faster, at 15.3% CAGR between 2021 and 2026. The MMA segment is growing fastest, projected at 12% CAGR through 2030. The post-COVID rebound has been stronger than most analysts expected.

How many martial arts schools are there in the U.S.?

IBISWorld counts over 72,000 martial arts studio businesses in the United States in 2026. No single firm holds more than 5% market share. The industry is highly fragmented and dominated by independent, owner-operated studios.

Is a martial arts gym profitable?

It can be, but margins are tighter than they look. Gross margins typically run 80–84% on services. Net operating margins depend heavily on rent, instructor payroll, and most critically, student retention. Studios with high churn (>10% monthly) frequently operate near break-even despite healthy enrollment. Those achieving 85%+ annual retention in their primary discipline tend to be genuinely profitable.

What is the fastest-growing martial art?

Brazilian Jiu-Jitsu (BJJ) is widely cited as the fastest-growing martial art globally. MMA overall is the fastest-growing combat sports category, driven by UFC viewership and the associated grassroots enrollment pipeline. In the female segment, kickboxing and Krav Maga are among the fastest-growing disciplines by participation rate.

What is the average revenue of a martial arts gym?

A typical studio needs approximately 187 students at $150 per month to cover the fixed overhead of around $22,441 monthly, assuming 80% gross margins. Average Revenue Per Member (ARPM) benchmarks suggest studios should target above $165 per month by 2027. Well-managed studios with 150–300 students and diversified revenue (private lessons, retail, events) can generate net profits of $50,000–$150,000 annually.

Which region has the fastest martial arts industry growth?

Asia-Pacific is the fastest-growing region, driven by ONE Championship’s expansion, cultural heritage in combat sports, and a rapidly expanding middle-class consumer base across India, Indonesia, Vietnam, and Southeast Asia. In the equipment sub-market, Europe is projected to post the fastest regional CAGR at 5.81% through 2030.